Apr 24, 2023 Market Commentary: The Fed’s Balancing Act

Equity markets have been trading sideways since Q3 2022, and market movements have been fairly subdued in the last few weeks. Since then, we have seen a plethora of data and even more speculation about what comes next. Fed policy takes time to sift through to consumer and business action, but we are finally starting to see some of the results now. Over the last 16 months, the Fed has raised interest rates from 0% to nearly 5%. This dramatic increase has had several known impacts today:

• Capital is more expensive, and less available. On the consumer side, mortgage rates are substantially higher, limiting buyer’s ability to qualify and desire to buy real estate. On the business side, companies are less willing to take out debt to build new buildings, hire new workers, and spend money on research and development. Future economic growth is at risk.

• Savers are being rewarded, at the expense of spenders. For the first time in a long time, savers are starting to see a return on their cash. Many high-yield savings accounts are yielding four percent or higher. Higher savings yields in combination with inflation means that spending money has become much more expensive. Consumer preferences are starting to change, whether by choice or by force. This has big implications for an economy that is 70% comprised of consumer spending.

• Assets and liabilities are mismatched. As bond yields have gone up, prices of bonds have come down, causing the asset class to have its worst performing year on record in 2022. Financial institutions with sizable bond positions have seen a rapid and substantial mismatch in the value of assets vs. liabilities. Banks can be particularly affected by this mismatch, as they may be forced to sell assets (i.e., bonds) at significant losses to meet demands for withdrawal.

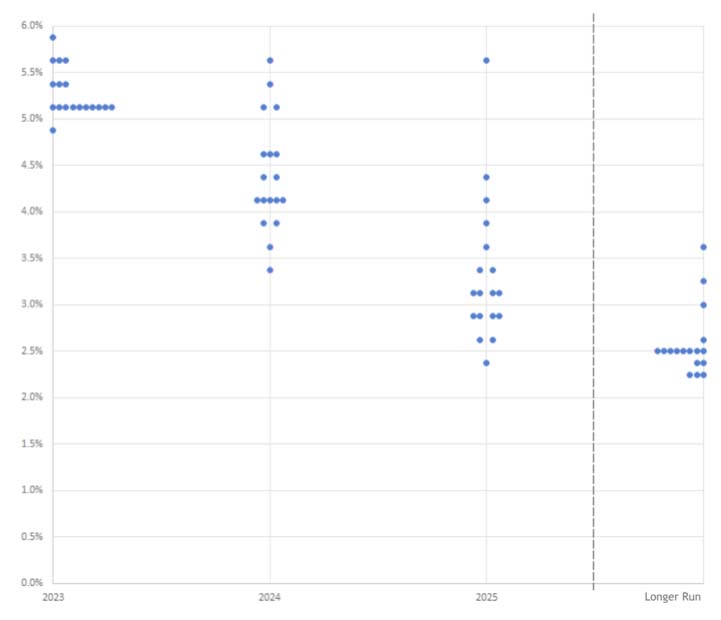

FOMC Participants’ Assessment of Appropriate Monetary Policy: Midpoint of Target Range or Target Level for the Federal Funds Rate

We now sit at a very important crossroads for Fed action. Although prices have come down from the peaks of 9%+, we are still nowhere near the target of 2%. The housing and labor markets have shown signs of slowing down but are not near any level of concern for the Fed. Evaluating these conditions alone in a vacuum suggests that Fed should continue their tightening approach – raising rates to lower inflation further. However, seeing the true effects of this rapid rise in interest rates will take time. The Fed may have already done enough to change consumer and business actions, slow down the economy, and lower inflation. If they raise rates further, we will likely see more cracks (like the regional banking crisis experienced a few weeks ago), leading to economic damage and slower growth in the long run.

The current Fed dot plot, which tracks FOMC participants’ assessments of appropriate monetary policy, shows that most believe we should have one more rate hike and no rate cuts this year. It is also important to note is that most believe we should get to around 2.5% in the long run (above the 0% we have been at for more than a decade – see our last commentary on “The End of Easy Money.”) This suggests the next bull cycle will look different from the last – the time of leveraging up to scale up margins is over.

The next Fed decision comes in the first week of May. Inflation, jobs, and housing data released over the next few months will give us a direction on where the market is going, and Fed Chairmen Jay Powell and the rest of the FOMC committee have some very difficult decisions to make on guiding the US economy. Buckle Up.

As always, please do not hesitate to reach out to your financial advisor with any questions or concerns.

The Seventy2 Capital Team

Commentary and Research provided by:

Michael Levitsky, CFA®, CAIA® – Director of Investment Strategy

Wells Fargo Advisors Financial Network did not assist in the preparation of this report, and its accuracy and completeness are not guaranteed. The report herein is not a complete analysis of every material fact in respect to any company, industry, or security. The opinions expressed here reflect the judgment of the author as of the date of the report and are subject to change without notice. Any market prices are only indications of market values and are subject to change. The material has been prepared or is distributed solely for information purposes and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Additional information is available upon request.

PM-08072025-6378146.1.1